IN THE basement of a hospital in Portland, Oregon, a sales representative spends 45 minutes scrolling through WhatsApp messages, searching for a photograph of an instrument tray. The surgery begins in 20 minutes. The correct implant—one of 70 variations for a single device—remains elusive. This scene, repeated thousands of times daily across America’s operating theatres, illustrates a curious paradox: medical-device firms have innovated themselves into operational paralysis.

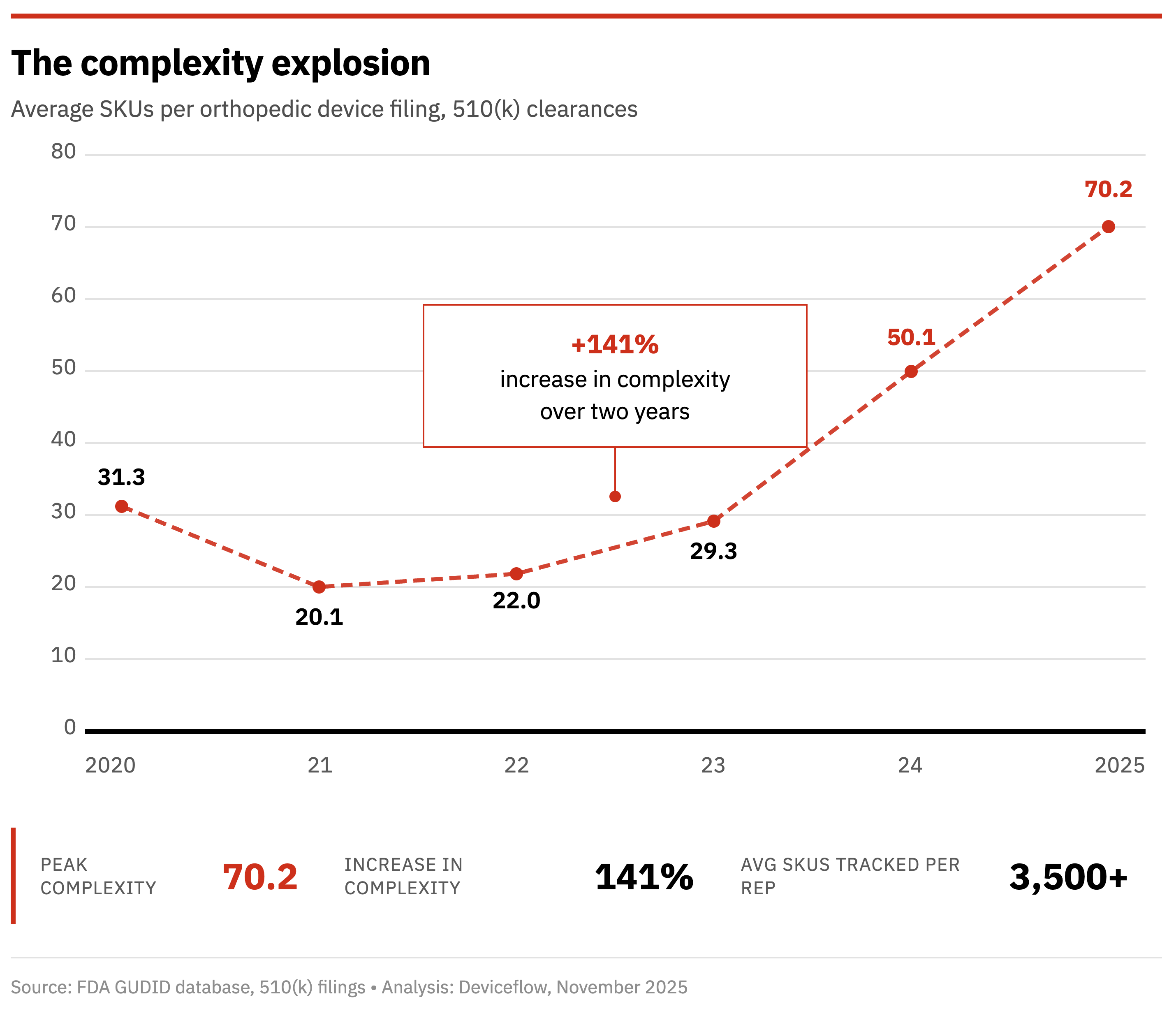

The numbers tell a startling story. In 2023, the average orthopaedic device required 29 stock-keeping units (SKUs) to accommodate various sizes, configurations and surgical preferences. Today that figure stands at 70—a 141% increase in complexity in just two years, according to analysis of America’s Food and Drug Administration database. The explosion shows no signs of abating.

This complexity comes at a price that few executives care to calculate. Medical-device companies already devote roughly 36% of revenues to selling, general and administrative expenses—a burden that would make even pharmaceutical executives blanch [1]. Top performers manage to contain these costs to 28.6% of revenues; laggards see them balloon to 34.4% [2]. For an industry where margins determine survival, this gap between winners and losers is widening.

The productivity paradox

Consider the mathematics of modern medical sales. The typical orthopaedic representative now tracks approximately 3,500 individual SKUs across multiple hospitals, surgical centres and storage facilities. They must know which items reside where, what expires when, which surgeon prefers which configuration, and what inventory sits on backorder. Left-specific implants must not be confused with right-specific ones. Instruments for posterior approaches must be distinguished from those for anterior ones.

Little wonder, then, that sales representatives spend a mere 28% of their working hours actually selling—a figure that would appal Henry Ford [3]. The remaining 72% disappears into what might charitably be called “administrative tasks”: photographing instrument trays, updating spreadsheets, managing preference cards, and engaging in the Sisyphean labour of inventory reconciliation.

The causes of this complexity explosion are manifold, each defensible in isolation yet collectively catastrophic. Surgeons, wielding considerable market power, demand bespoke configurations. Hospitals, squeezed by their own cost pressures, insist on unique packaging arrangements. Regulatory requirements spawn endless variations. Competition drives feature proliferation—what economists might recognise as a classic arms race where everyone runs faster merely to stand still.

Innovation’s dark side

Product teams, incentivised to launch new offerings, celebrate each successful 510(k) clearance. Sales teams, meanwhile, inherit the operational burden. This misalignment of incentives—where those who create complexity bear none of its costs—would be familiar to anyone who has studied the theory of externalities. The product manager who adds “just one more size variation” rarely witnesses the representative who misses a surgery because the correct implant cannot be located.

The trajectory appears unsustainable. In 2022, managing 22 SKUs per device seemed reasonable. By 2023, the number had grown to 29. Now at 70, the system creaks under its own weight. Extrapolation suggests a future that is plainly absurd, yet no mechanism exists to arrest the progression [4].

The hidden costs multiply relentlessly. Inventory carrying charges escalate with each SKU addition. Training requirements expand geometrically—every variant demands documentation, instruction, and troubleshooting protocols. Error rates climb. The industry’s 25% annual turnover in sales personnel, largely attributed to operational frustration, imposes recruitment and training costs that rarely appear in official calculations [3].

Most damning is the opportunity cost. Hours spent managing spreadsheets are hours not spent with surgeons. Relationships atrophy while representatives wrestle with logistics. Competitors who solve this puzzle will claim market share from those who do not.

Why conventional remedies fail

The standard corporate response—“hire more people”—merely shifts the problem. Additional headcount to manage complexity creates more communication nodes, more coordination challenges, more opportunities for error. Moreover, 85% of sales leaders report difficulty securing budget for necessary personnel [3]. The era of throwing bodies at problems has passed.

“Better training” presumes ignorance where systemic failure exists. Representatives understand inventory management perfectly well; they lack tools fit for purpose. One might as well train a mediaeval scribe to work faster rather than provide a printing press.

“Process standardisation” offers false comfort. Standardising chaos yields only consistent chaos. No amount of procedural refinement can tame exponential complexity.

The automation imperative

Forward-thinking companies are treating operational infrastructure with the seriousness once reserved for product development. They recognise that competitive advantage no longer resides solely in titanium and surgical steel but in the invisible systems that deliver these products efficiently.

The solution is not another dashboard—representatives already suffer from application fatigue. Rather, intelligence must be embedded within existing workflows. Image recognition can identify SKUs from photographs. Machine learning can predict inventory requirements. Real-time synchronisation can update preference cards across facilities. None of this requires representatives to master new software.

Amazon’s warehouses offer an instructive parallel. The e-commerce giant does not expect workers to memorise the location of millions of products. Neither should medical-device companies demand such feats from their sales forces.

A closing window

External pressures compound internal challenges. America’s Centres for Medicare & Medicaid Services have introduced prior-authorisation requirements that add layers of administrative complexity. Margins face compression from multiple directions. Companies attempting to navigate these waters with WhatsApp and Excel spreadsheets are steering towards the rocks.

Yet crisis breeds opportunity. While competitors drown in complexity, those who solve the operational puzzle will capture disproportionate rewards. The mathematics are elementary: every hour a representative spends on inventory management is an hour a competitor might spend building surgical relationships.

The medical-device industry stands at an inflection point. The next decade’s winners will not be determined solely by product innovation—a game everyone plays with diminishing returns. Victory will belong to those who recognise that 70 SKUs per device demands 21st-century operations, not 20th-century workflows. The companies that fail to adapt will discover, too late, that they have innovated themselves into irrelevance.

Sources

[1] AdvaMed (2015). Medical Device Industry Cost Structure Analysis.

[2] Roland Berger (2024). Taking the Pulse After the Pandemic: Global MedTech.

[3] Salesforce (2024). State of Sales Report, 5th Edition.

[4] FDA GUDID Database & 510(k) Filings Analysis (January 2025).

[5] KPMG (2023). Medical Device Inventory Management: Optimizing Working Capital.