The Quiet Revolution in Medical Device Innovation

Something fundamental has shifted in the medical device industry, and most people haven’t noticed yet. While the headlines still focus on Boston Scientific’s latest acquisition or Stryker’s quarterly earnings, the real innovation story is happening elsewhere—in companies with fewer than 10 devices on the market, many on their very first FDA clearance.

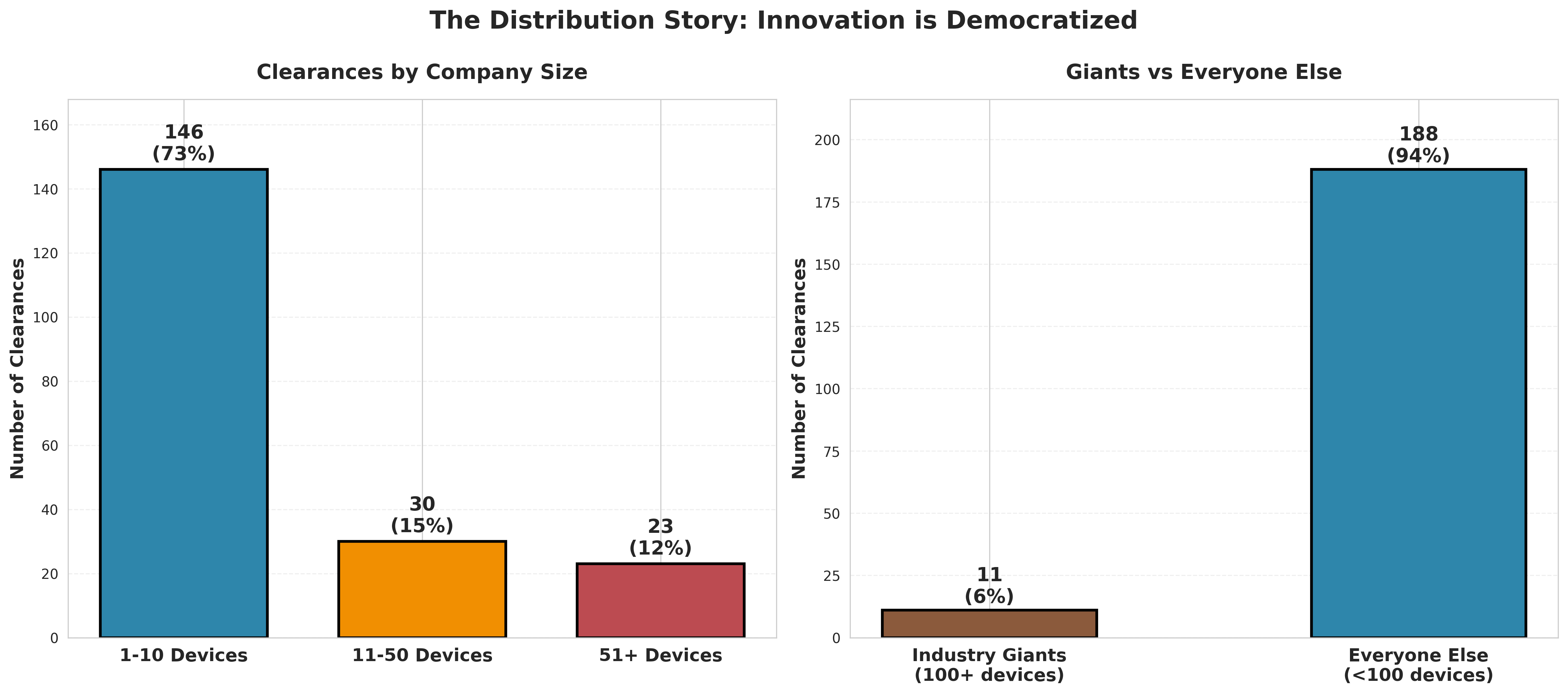

In October 2025 alone, approximately 199 new medical devices received FDA 510(k) clearance, a number that might seem routine to industry veterans. But here’s what should make every distributor, investor, and industry executive sit up: 73% of these clearances are coming from companies with fewer than 10 devices in their portfolio. Some are achieving their very first clearance. We’re not talking about minor accessories or me-too products—these are surgical systems, diagnostic tools, implants, and monitoring devices that could fundamentally change clinical practice.

This isn’t just a statistical anomaly. It’s proof of a tectonic shift in how medical device innovation happens, who drives it, and what it means for the entire go-to-market ecosystem.

The Death of the Traditional Innovation Model

The established playbook is dying, and the numbers prove it. Pharmaceutical, biotech and health care companies often report SG&A expenses of 40%–50% or more, with medical device companies facing similar pressures. When you’re burning half your revenue just to maintain operations, innovation becomes a luxury you can’t afford.

Large orthopedic companies have made their choice: They’re pursuing mergers and acquisitions to take advantage of economies of scale and tax inversions to lower their corporate tax rates, rather than investing in breakthrough technologies. As Tiger Buford astutely observed, “Big Ortho has abandoned true innovation in exchange for control, safety, and predictable 5% growth.”

This creates what I call the “innovation vacuum”—and nature, as they say, abhors a vacuum.

When the giants are cutting R&D while smaller players are doubling down, the innovation equation becomes clear: size isn’t an advantage anymore—it’s a liability.

The New Innovators: Who They Are and Why They Matter

The companies driving this innovation wave don’t fit the traditional mold. They’re lean, focused, and unburdened by the operational complexity that plagues larger players.

The Operational Advantage of Being Small

Here’s what the established players don’t want to admit: their size has become their weakness. Consider the operational burden:

- Sales reps spend just 28% of their week actually selling, with the majority of their time consumed by other tasks like deal management and data entry

- Sales teams use an average of 10 tools to close deals, with 66% of sales reps saying they’re overwhelmed by the number of tools

- Research shows 72% of sales representatives’ time is wasted on non-selling activities

When your sales force is spending less than a third of their time actually selling, and your SG&A is eating up half your revenue, innovation isn’t just difficult—it’s mathematically impossible.

The Distribution Dilemma: A $100 Billion Opportunity

This shift creates an unprecedented opportunity—and challenge—for the distribution ecosystem. The cost of distribution in medical devices can easily exceed 50% margin for marketing and sales, whether through OEM partnerships or strategic distribution agreements.

The Commission Structure Reality Check

The economics of medical device distribution are brutal:

- Independent reps typically work on a 25% straight commission

- Distributor commission rates typically range from 25% to 35% for disposables

- Direct sales models aren’t necessarily better: The true expense of a W-2 rep in the medical industry today begins with a fixed cost of $100,000

But here’s the critical insight: whether you’re paying 30% to distributors or maintaining a direct sales force at comparable cost, the real problem isn’t the commission structure—it’s the operational inefficiency that keeps reps from actually selling.

Why Traditional Go-to-Market Models Are Breaking

The traditional medical device go-to-market playbook assumed a world of concentrated innovation, predictable product cycles, and relationship-based selling. That world no longer exists.

The Value Analysis Committee Reality

The days of a single surgeon making a purchasing decision are over. Now, every new product must pass through a Value Analysis Committee (VAC), which includes clinicians, administrators, finance, and supply chain managers. This fundamental shift means:

- Sales cycles that stretch months or even years

- Multiple stakeholders with competing priorities

- Data requirements that go far beyond clinical efficacy

- Economic justification that rivals clinical outcomes in importance

For emerging manufacturers with limited resources, navigating this complexity without established relationships is nearly impossible. For distributors, it represents an opportunity to differentiate through expertise rather than just territory coverage.

The Competitive Dynamics Nobody Wants to Discuss

Here’s what keeps me up at night: the entire industry is organized around the wrong competitive axis. Everyone’s fighting over commission points and territory rights while missing the real battleground: operational efficiency and innovation access.

The Automation Imperative

Medical device companies are adopting systems that let them move quickly without compromising quality while maintaining compliance. The winners won’t be those with the lowest commissions or the largest sales forces—they’ll be those who solve the operational burden that keeps reps at 28% productivity.

Consider what’s already happening:

- AI systems can process thousands of medical images in seconds—a task that could take human specialists several days

- 3D product demos enable sales representatives to virtually showcase products in their actual size, eliminating the requirement to transport physical devices

- Mobile-first dashboards provide instant access to product specifications, inventory status, and customer preferences

The companies that embrace this operational transformation—whether manufacturers or distributors—will capture the value currently being destroyed by inefficiency.

The Strategic Implications for Every Stakeholder

For Distributors: The Race for Emerging Partners

The opportunity is clear but time-bound. With 73% of clearances coming from smaller companies, the traditional approach of waiting for proven winners won’t work. By the time a company has proven market traction, they’ve either been acquired or established their own distribution.

Action items:

- Develop systematic FDA clearance monitoring to identify emerging technologies

- Build evaluation criteria that go beyond traditional metrics

- Create partnership models that work for pre-revenue companies

- Invest in the operational infrastructure to support multiple emerging brands

For Manufacturers: The Existential Choice

Emerging manufacturers face a brutal reality: Nearly three-quarters of independent medical sales reps have had substantial medical sales experience, with two-thirds having held positions in medical sales management. You’re competing for the attention of highly experienced professionals who have plenty of options.

Critical decisions:

- Partner early with distributors who can navigate the VAC complexity

- Focus on data and economic value from day one

- Build products that solve operational problems, not just clinical ones

- Accept that distribution will cost 40-50% regardless of the model—optimize for reach and expertise instead

For Investors: Rethinking the Value Equation

The traditional metrics for evaluating medical device companies are obsolete. Market cap and revenue multiples matter less than innovation velocity and operational efficiency.

New evaluation criteria:

- Time from concept to clearance

- Operational burn rate relative to development progress

- Distribution partnership quality over territory coverage

- Data and evidence generation capability

- VAC navigation expertise

The Uncomfortable Truth About Industry Transformation

The medical device industry is experiencing what I call “innovation democratization,” but that’s only half the story. The other half—the part nobody wants to discuss—is that the infrastructure hasn’t caught up.

We have:

- More innovation than ever, trapped in companies without distribution

- Distributors desperate for differentiation but stuck in territory battles

- Sales reps burning 72% of their time on non-selling activities

- Established players protecting margins instead of driving innovation

- An entire ecosystem optimized for a world that no longer exists

The Path Forward: Embracing the New Reality

The solution isn’t to fight this shift—it’s to embrace it and rebuild the infrastructure to match the new innovation landscape. This means:

1. Accepting the New Innovation Geography

Innovation isn’t coming from where it used to, and it’s not going back. The U.S. FDA has traditionally been seen as more supportive of innovation, and has implemented processes to help smaller companies and startups get their products efficient market clearance. The regulatory environment actually favors the innovators now.

2. Rebuilding the Go-to-Market Infrastructure

The current model where reps spend 28% of time selling is unsustainable. We need:

- Automation of administrative tasks

- AI-powered territory and account planning

- Integrated systems that eliminate tool proliferation

- Commission structures that reward efficiency, not just volume

3. Creating New Partnership Models

The traditional manufacturer-distributor relationship assumed stable products and predictable markets. We need models that work for:

- Pre-revenue companies with breakthrough technology

- Rapid iteration and product evolution

- Data-driven selling to VACs

- Shared investment in market development

The Clock Is Ticking

Every month brings another ~200 FDA clearances, with 146 coming from companies most distributors have never heard of. Each represents a potential breakthrough, a possible partnership, a future market leader. But they also represent a ticking clock.

Medical device manufacturers face several key issues including cybersecurity regulation, risk mitigation, and supply chain resilience. The companies that can navigate these challenges while maintaining innovation velocity will define the next decade of medical technology.

For established players clinging to the old model of predictable 5% growth and operational inefficiency, the message is clear: the barbarians aren’t at the gate—they’re already inside, and they brought FDA clearances.

For everyone else—the distributors seeking differentiation, the manufacturers seeking scale, the innovators seeking partners—this is your moment. The innovation pipeline has been democratized. The question isn’t whether you’ll adapt to this new reality, but how quickly you can capitalize on it.

The medical devices are getting cleared. The innovation is accelerating. The old guard is retreating into financial engineering and “safe” growth.

Who’s going to bring the future to the bedside?

The analysis in this piece is based on FDA 510(k) clearance data through October 2025, industry financial reports, and extensive research into medical device distribution models. The shift toward distributed innovation isn’t a prediction—it’s a measurable reality that’s accelerating every quarter. The only question is whether the industry’s infrastructure will evolve to support it, or whether we’ll continue to operate with models designed for a world that no longer exists.