For three decades, competitive advantage in orthopedic medical devices meant the device. Better materials, better geometries, better instrumentation, better outcomes. Companies spent millions on R&D and competed on what they made.

That era isn’t over, but its primacy is.

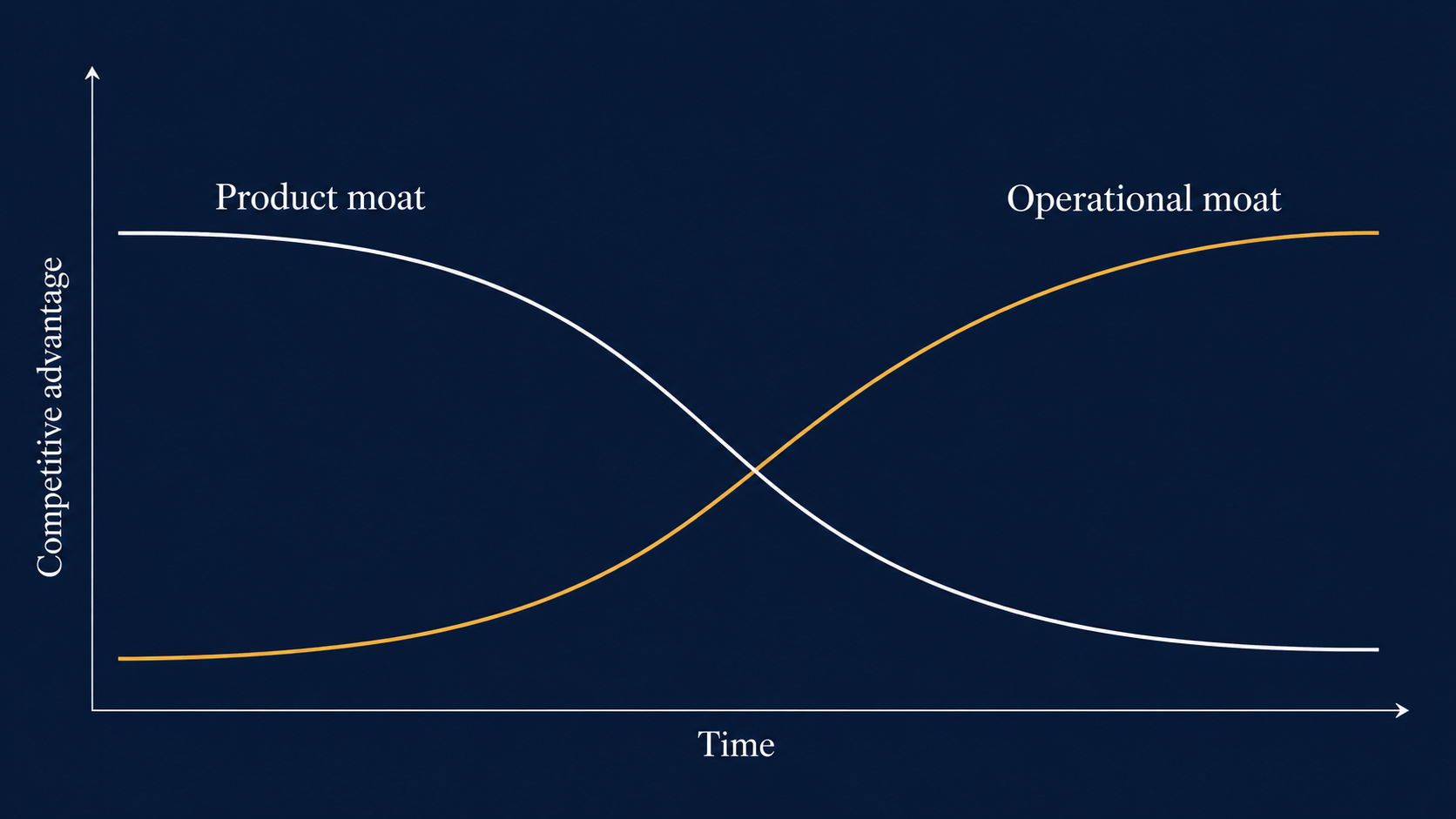

Surgeons today increasingly select implants based on familiarity, availability, and what their hospital already stocks rather than meaningful clinical differentiation. The competition is rotating away from the device and toward everything around it. That changes how medical device manufacturers and distributors should be allocating capital, and it changes which independent rep relationships are worth fighting for.

The narrowing product moat

The U.S. orthopedic device market hit $39.6 billion in 2023, representing 67% of the $59 billion global market and growing at 6.3% annually (ORTHOWORLD 2024 Annual Report). The structure is concentrated at the top: fewer than 50 companies exceed $100 million in revenue, and seven companies over $1 billion generate $39 billion of the total. Below that line, hundreds of independent manufacturers fight for share inside a category that any classical strategy framework would recognize as mature.

When the fundamental product becomes commoditized, differentiation migrates outward to service, distribution, financing, and operational ease. Semiconductors went through it. Commercial banking went through it. Orthopedics is going through it now.

The evidence is in how purchasing actually happens. Surgeons develop preferences early in their careers and rarely switch unless something operational forces the decision. Hospital value analysis committees increasingly evaluate devices on total cost of ownership: implant price plus the burden of managing the vendor relationship. ASC administrators, running lean operations with three to five staff, select manufacturers based on who creates the least administrative drag.

A KPMG analysis of medtech commercial models put it plainly: “Economic benefit value props are becoming almost as important as clinical efficacy” in device purchasing decisions (KPMG, 6 Key Challenges for Medtech Sales Growth, 2022). Product innovation still matters at the margin, and breakthrough technologies like robotic platforms and novel biologics still represent real differentiation. For the rest of the volume, the device is table stakes. The competition has moved downstream.

Three operational levers

If the product moat is narrowing, what’s widening? Three operational advantages, none of which require a bigger R&D budget.

1. Speed-to-revenue

The manufacturer whose case-to-cash cycle runs in days instead of months operates with a fundamentally different financial profile. Working capital improves and reinvestment accelerates, and there’s a second-order benefit that’s bigger than either: independent reps and distributors prefer to work with the companies that pay them promptly.

The distributors who understand this are making it explicit. Recently a distributor founder we work with described the rep payout cadence they’re building toward:

“We want our reps paid in 48 to 72 hours. That’s part of the sell.”

— Founder of a multi-line orthopedic distributor

That’s the rep economics rotating in real time. The manufacturer or distributor with the fastest, cleanest payout becomes the preferred partner, regardless of where their product sits in the implant comparison.

The industry standard for case-to-payment runs 60 to 90 days, and many manufacturers stretch beyond 120 when billing disputes push invoices into extended AR cycles. Pricing errors alone account for 2 to 5 percent of total revenue at organizations without robust pricing controls (Improving Pricing Accuracy in Medical Devices, 2020). For distributors, where unbilled cases compound the problem, leakage runs higher.

Compressing the cycle isn’t theoretical, but it does require eliminating the manual translation steps between field communication and the system of record. That’s the same gap that costs mid-market distributors $150,000 to $220,000 a year in reconciliation labor alone, and the return is asymmetric: faster payment creates rep preference, which drives case volume, which improves unit economics. The advantage compounds with every case.

2. Operational transparency

When a distributor can see order status, commission accruals, and inventory position without making a phone call, the single largest source of channel friction disappears. The rep stops mediating between the manufacturer and the back office, and the ops team stops fielding inquiries instead of processing orders.

The flip side of that gap, from the manufacturer perspective, came up in a recent conversation with a commercial leader at a mid-market device manufacturer:

“I’ve got hundreds of distributorships I work with, and no proper way of structuring this communication. It becomes messy so quick with just one or two messages.”

— Commercial lead at a mid-market medical device manufacturer

That’s the manufacturer side of the same problem: every distributor relationship is a partial picture, stitched together across email threads and text messages and phone calls. Nobody has the full case-flow in one place.

Field inventory shows the problem in stark form. Most companies have millions in consignment and loaner inventory with location accuracy under 70% when relying on manual tracking (Terso Solutions, 2020) — not because anyone’s negligent, but because the systems they bought a decade ago require the same reps running between surgical cases to also do manual cycle counts. Field reps already spend 30 to 40 percent of their time on administrative coordination (Curvo Labs, Hip and Knee Implant Review, 2023).

The distributors improving visibility aren’t asking reps to do more. They’re capturing the signals that already exist (delivery confirmations, text messages, case completion notifications) and turning them into real-time inventory maps without asking the field to change behavior.

3. Partner density

The third lever is structural. Zimmer Biomet’s CEO Ivan Tornos is converting the company’s 2,500-person U.S. salesforce, roughly two-thirds 1099 contractors at the start of 2026, to a fully dedicated and specialized model by the end of 2027 (MedTech Dive). His rationale, in his own words: competitors with fully dedicated, specialized salesforces are more productive. Independent manufacturers can’t match that buildout on breadth alone, but they can coordinate.

By partnering with adjacent, non-competing manufacturers, an independent distributor can offer hospitals a competitive total portfolio across trauma, spine, biologics, and extremities. No single manufacturer owns all of it, but the distributor walks in with a comprehensive solution, which is what hospital procurement increasingly demands.

This network strategy is unavailable to manufacturers still thinking in direct salesforce terms. It requires shared visibility into case flow, standardized order processing, and transparent commissions across lines. Partner density is a competitive advantage built entirely from operational architecture.

The invisible P&L problem

The strategic shift toward operational competition runs into a measurement problem: most of the costs that operational excellence eliminates don’t show up as discrete line items.

The cost of manual order reconciliation isn’t in cost of goods sold. It isn’t labeled in SG&A. It’s distributed across four or five salary lines, assorted software subscriptions, and an unknowable amount of opportunity cost: billing disputes that take 45 days to resolve, revenue that leaks from cases completed but never properly invoiced, new product lines the team couldn’t onboard because everyone was buried in last month’s reconciliation backlog.

For a mid-market distributor doing $20 million in annual revenue, the aggregate hidden cost runs $600,000 to $1,300,000 a year. It’s not visible because it’s always been there, predating the current team and the current systems and the current leadership. Eliminating it requires first seeing it, and seeing it requires asking a question most organizations never think to ask: what percentage of our operations team’s time is spent translating between communication formats rather than doing work that requires their actual expertise?

The bifurcation

The medical device distribution market is bifurcating, and the split is operational.

On one side: companies running on the email-and-spreadsheet infrastructure they built a decade ago, adding headcount linearly as volume grows, competing on relationships that are one retirement away from disappearing. On the other: companies that have closed the gap between field communication and their systems of record. They process three to five times the order volume with the same team, pay reps faster, invoice cleaner, and win new manufacturer lines because their operational data is visible in real time. A manufacturer evaluating distribution partners can see exactly how cases flow through the organization before signing anything.

The gap will widen every quarter. Not because of AI hype, but because of operational mathematics. The distributor who processes a $50,000 case and invoices it the same day has a fundamentally different cash conversion cycle than the one who takes 60 days, and across hundreds of cases per month that difference becomes a structural advantage that’s very hard to overcome through sales effort alone. BCG estimates generative AI can automate 20 to 30 percent of administrative work in healthcare operations (BCG, Medtech Companies Must Move Faster on GenAI, 2023) — for order processing in this industry specifically, that number is conservative.

The leaders inside the majors are saying the same thing in different words. From a recent conversation with an operations executive at one of the orthopedic majors:

“We should be measuring the throughput time in hours, not in days, not in months.”

— Operations executive at a top-five orthopedic manufacturer

When the largest companies in the category are setting the benchmark in hours, the distributors and manufacturers measuring themselves in weeks aren’t competing in the same market anymore.

Zimmer Biomet’s salesforce conversion is one response: a top-of-market company reshaping its commercial model, betting that specialization at scale beats network breadth. For the thousands of independent manufacturers and distributors who collectively represent most of the long tail, the response looks different. The win isn’t in salesforce size but in the speed and accuracy with which a case moves from the surgeon’s hands to the manufacturer’s books.

Over the next twelve months, the operational layer becomes the competitive layer. The companies that recognize this are already moving, and they’re already showing up in their own numbers.

What percentage of your ops team’s time this week was spent translating between formats rather than doing work that requires their judgment?